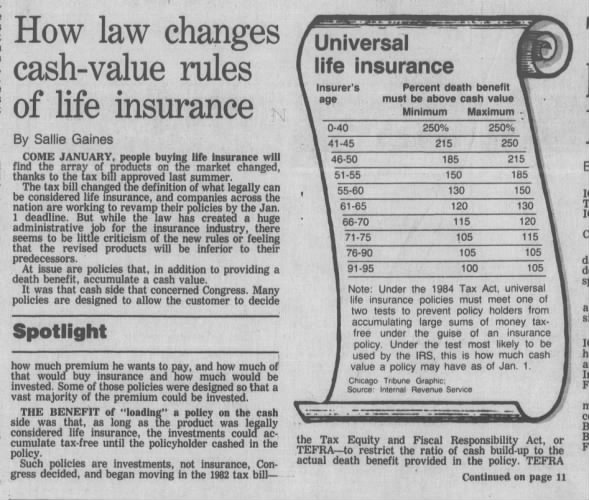

Cash Value

Cash Value (Account Value)

This creature called universal life has evolved from a combination of term insurance and a flexible premium annuity to a range of differing products with various design features.

Common to any of these variations is the fact that future cash values cannot be determined completely at issue.

Cash values (and other benefits) are produced by a formula that is specified in advance. Some of the various elements used in the formula,however, can be adjusted after issue by the insurer. 6. THE CONCEPT OF THE BENEFIT GENERATING ACCOUNT

We have mentioned several times that the function of the account value

is to determine future benefits.

1983 – UNIVERSAL LIFE VALUATION AND NONFORFEITURE: A GENERALIZED MODEL, Society of Actuaries

Traditional plans are fairly simple in their structure. One can look at their premiums, their cash values and their dividends, if there happen to be any.

Universal life presents something of a paradox. –BEN H. MITCHELL

1981 – Universal Life, Society of Actuaries

Blumenthal v New York Life – Cash Value What else is it supposed to be

Blumenthal v New York Life – Cash Value What else is it supposed to be

2017/2/17 – LIBGWG Conference Call – “Gary Sanders (National Association of Insurance and Financial Advisors—NAIFA) agreed that use of the term “cash value” was confusing.”

The primary purpose of the policy’s Cash Value is to fund the Cost of Insurance.1999 – Suitability, Dearborn Continuing Education

A cash value is therefore by definition a savings account whether we choose to call it that or not. — MR. ALAN RICHARDS <EF Hutton>

1981 – THE FUTURE OF PERMANENT LIFE INSURANCE, Society of Actuaries

Despite the fact that there are cash values in the thirty‐year term contract, from a consumer’s viewpoint it has no savings element.

All of the premium is required to provide the thirty years of protection.

The savings element in the thirty‐year endowment is the difference inthe premiums of the two contracts.

1973 – PRICE DISCLOSURE AND COST COMPARISON, Society of Actuaries

“Cash value policies differ from term insurance in three important ways.

-First, the premiums for a cash value policy are initially much higher than for term insurance for the same amount of insurance protection.

-Second, unlike the premiums for term insurance, cash value premiums do not go up with age, but remain the same throughout the payment period.

-Third, these insurance policies develop cash values which increase each year.”

1979 – GOV – Small business problems with insurance Part 1, Government Hearing

“Cash values, which are the residual amounts of prefunding reserves returned to policyholders if the contracts are terminated, are secondary benefits.” Technical Resource Group <Industry>

1994-1, NAIC Proceedings

ACADEMIC2004, AP UNIVERSAL LIFE INSURANCE – ASPECTS OF THE CASH VALUE DEVELOPMENT, Martin Birkenheier, 146p

Government Hearings

1978 – GOV – Life Insurance Marketing and Cost Disclosure Report – Moss 106p

1983 – GOV – Tax Treatment of Life Insurance

FEDERAL LAW AND LEGISLATION, NATIONAL ASSOCIATION OF

LIFE UNDERWRITERS <NAIFA / NALU>, p314

MEDIA